Wow. I’ve been waiting for this project for 5 years.

Is it possible? I hesitate to share all the details with you (since I know that’s a jinx!), but I’m so excited, I can’t quite shush myself.

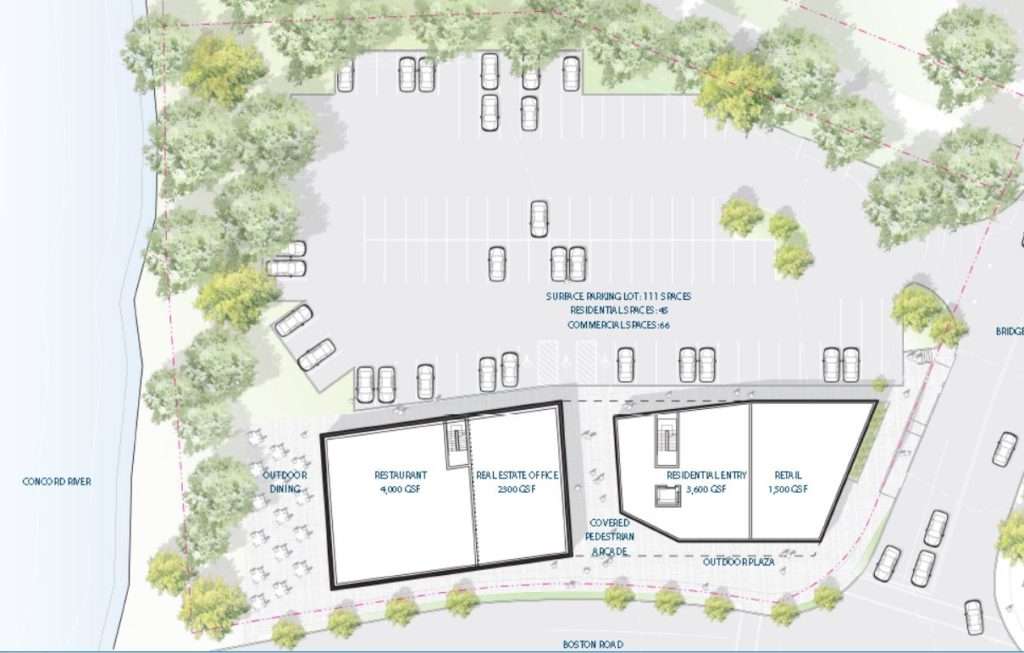

Initial Site Design

There comes a moment in every real estate investor’s life when they want to lance the Great White Whale (thanks Moby Dick, a solid 4 chapters ONLY describing how “white the whale” was… geesh).

I had been following this parcel for 5 years, and it went under agreement twice, with big commercial developers, that I knew I had no chance of beating. But then – one by one – they backed out, one since they couldn’t get a drive through approved, and the other, being they couldn’t get their retail anchor tenant they wanted, to commit.

As I’d been working very closely with the economic development team in this town, they called me to inform me the property was available again – and I immediately didn’t waste a SECOND this time.

Have you ever had moments, where you hesitated – and the opportunity is gone? I’ve had plenty. Thus, the whole tagline in my office (#ShutUpAndDoIt!)…but this time, I jumped in.

And – it just so happens, that over the last 5 years, the town was doing everything it could to foster development, including, a zoning overlay, right in this very spot.

I truly feel, that as of now (still going through feasibility and due diligence!), we have the RIGHT location, at the RIGHT time, with the RIGHT team, and the RIGHT government to make this work.

And, in case you haven’t heard by now… I’m super, super excited. Condos on top, Restaurant, Retail and Office on Bottom – OUR office. And a Restaurant I’ve personally chosen. On Riverfront. At a busy intersection and a very visible “gateway” to the town. With parking and tax incentives. And Bonus depreciation. And… well, you see why I’m excited.

We’ll most likely be looking for partners and other possible relationships with folks on this one – if you’re interested, send an e-mail to me , and we’ll be sure to talk and see if it’s the right fit!

In an upcoming post – I’ll let you know how we run due diligence on a project like this – even I need to get out of my comfort zone every once in a while!

Ready to give up after your first direct-mail piece yielded no results? AARE Director of Acquisitions and Resales, Rob Reutzel shares that marketing is a numbers game that requires persistence and patience.

The average response rate for direct mail is 2-3% AND that number increases exponentially with each subsequent “touch” or communication from you, so follow up, follow up, FOLLOW UP!

Consistency for at least 12 months is key. So don’t give up and fail forward fast. Watch Rob’s video for more:

https://aarealestategroup.com/wp-content/uploads/aa_real_estate_logos_final_group-300x112.png00Matt Perryhttps://aarealestategroup.com/wp-content/uploads/aa_real_estate_logos_final_group-300x112.pngMatt Perry2017-02-09 18:44:482017-02-09 23:11:29Marketing Realities for Real Estate Investors

OK, listen. I know that politics by itself is a nasty topic right now. And nevermind that I’m about to propose an opposing opinion to the National Association of Realtors. But, as a real estate professional and an economist, and always a student of causality, I want to weigh in on this.

Any article or media post that you are reading, with homeowners saying “In the first 24 hours Trump was in office, he already cost me $400 this year,” is just a false statement. And I get SO ANGRY when people, namely the mainstream media, put out sound bites or opinions and call it news. So, here’s what ACTUALLY happened, folks.

First of all, let’s review what an FHA mortgage is — FHA is the Federal Housing Administration, which was created to insure mortgages and collect fees from borrowers to reimburse lenders in case of a default. They are attractive to borrowers, particularly from a credit-worthiness standpoint, because they are easier to qualify for and require a down payment as little as 3.5% of the purchase price, plus closing costs and a monthly MIP (mortgage insurance premium).

From 2006 to 2009, there was not enough in the FHA reserve to bail out all the banks staggering under defaulted loans. In response to that, the US Treasury just printed money like there was no tomorrow ($1.7 BILLION, to be exact) to keep the FHA funded, and therefore the banks didn’t learn their lesson — see my previous write-up on The Big Short. After this debacle, FHA premiums rose significantly — in 2013, FHA borrowers paid 1.75% as an up-front fee at closing, and an additional 1.30-1.35% of their total purchase price over 12 months as mortgage insurance premium (MIP) in addition to their monthly mortgage payment. The purpose of these payments is for the FHA to replenish it’s cash reserves since the crash completely wiped it out — just to keep the banks with terrible underwriting guidelines and more concern for profit than potential risk afloat, which in the end, wasn’t at risk at ALL (again, see my Big Short article!), but I digress.

So. On Jan 10 — just ten days before leaving office, the Obama administration, in what some have called a political move to boost public opinion and ratings on the way out — made an announcement that effective Jan 27, they would maintain the 1.75% premium cost at closing, but would cut the MIP, currently at 0.85% of the purchase price, down to 0.60%, saving NEW homeowners closing after Jan 27 an average of $400 a year. It does NOT “cost” current homeowners/borrowers anything, since nothing changed for them after Trump halted the lowering of this premium — perhaps a lost DISCOUNT, but no added costs for borrowers.

So why did the Trump administration suspend this discount to new borrowers? As I drafted this article, the only official statement is: “FHA is committed to ensuring its mortgage insurance programs remain viable and effective in the long term for all parties involved, especially our taxpayers,” and the new HUD Secretary, Ben Carson, added he would “work with the FHA administrator and other financial experts to really examine that policy.”

I think putting more thought behind this, instead of just enacting more “feel good legislation,” is prudent, especially where — and this is my “well informed” opinion for sure — all signs are pointing to a correction in the marketplace, yet again. We’re seeing it here in the tremendous uptick in our short sale firm, where we are now getting 4-5 new incoming cases a week, an uptick from our usual pace of 1-3 new cases per week, mostly due to job loss or reduction in income. Income and employment have not seen increases in line with the increases in the price of housing, which is a primary indicator for when we’re due for a correction.

THAT said, if we are in for another correction, banks will be looking to the FHA for bail-outs when defaulting mortgages increase as people can no longer pay their high mortgage payments (if they were even credit-worthy to begin with), and the FHA relies primarily upon the fees it collects from borrowers to bail them out. If there’s no money left, well then, one could assume another total obliteration of banking as we know it. But since no one learns from history, if the FHA runs out of money the most likely scenario is that we, the taxpayers, will bail out the big banks, literally giving them ZERO risk in making these bad loans. Hell, they should just start issuing sub-prime loans again, since none of this does anything for accountability anyway! In that case, since the facts and economic indicators apparently don’t matter, they should just go ahead and decrease the MIP and save everyone $400 a year.

All sarcasm aside, I have to say it’s an encouraging sign for the FHA to keep the rates stable until they complete an economic analysis (like any insurance company or prudent financial firm would) as to how much risk they’d be exposed to in the event of a mortgage collapse, make sure they have sufficient reserves, and THEN make the adjustment.

Or they could just get rid of it altogether, since it won’t matter and the US Treasury will just print more money and bail out the banks anyway!

: – P

End of rant, and thanks for reading. And remember, confirm the accuracy of where you’re getting your “facts.” Note: if it’s the media or a National Association, or anything else poised to make a profit from swaying opinion one way or another, better check multiple sources!

https://aarealestategroup.com/wp-content/uploads/Screen-Shot-2017-02-01-at-11.27.11-AM.png125125Nick Aalerudhttps://aarealestategroup.com/wp-content/uploads/aa_real_estate_logos_final_group-300x112.pngNick Aalerud2017-02-01 16:41:102017-02-01 16:41:10A Second Look at Trump’s Halt to Lowering Premiums

Sales is the million dollar skill and closing is the epitome of making a sale.

Are you closing at least 3% of the deals from people who respond to your marketing? Do you talk to at least 5 sellers a day? This may be the biggest thing holding back your business.

Want to learn more? Then AARE Director of Acquisitions and Resales, Rob Reutzel has some suggestions for you!

https://aarealestategroup.com/wp-content/uploads/aa_real_estate_logos_final_group-300x112.png00Matt Perryhttps://aarealestategroup.com/wp-content/uploads/aa_real_estate_logos_final_group-300x112.pngMatt Perry2016-12-15 15:20:332017-02-09 23:11:57Sales 101: Can You Close?

Let’s just get one thing straight — anyone who’s in the real estate business — whether they’ve done one, 100, or perhaps hasn’t even completed their first deal yet — we’ve all experienced REJECTION.

And not just a solid “NO.” LOTS of stuff like this:

“Who the *%#! are you?? How did you get my number? I’m calling the cops!” or,

“I would have to be an absolute buffoon to accept that offer. Who do you think you’re dealing with?” and my personal favorite,

“I’ve got a 9mm pistol with your name written all over it if you contact me again.”

Yikes! And then there’s the WORST kind of NO — the one that disguises itself as a YES — which you only uncover after hours and possibly days of follow up — sometimes EVEN AFTER you have a signed contract — where the seller just drops off the face of the Earth. In fact, we just had a deal where the sellers, after responding to our marketing and weeks of follow-up, finally agreed to meet, knowing they had to act before the foreclosure auction date. They didn’t use e-mail, and instead required us to drive to their home (about 40 minutes each way, ALWAYS in rush hour) 3 separate times, to get paperwork signed. And after we got it all signed? Nothing. They stopped replying to calls, e-mails, etc. Frustrating.

Or there’s the 6-unit building I had under agreement, all set to close the next day. The seller was one of those who owned the building free and clear, and just wanted enough to buy a trailer and live off the grid where he could prepare for the apocalypse. He wanted NO US dollars at closing — instead, we had to pay him $15K in gold coins that ONLY “Jeffrey down the street at ABC Coin Store can git, dropped in a paper bag with my name on it.” My closing attorney laughed, but we had it all set to go — until 3 hours before the closing, when he had a mental breakdown and threatened to kill his tenants and himself if we moved forward with the closing. Needless to say, I rarely hold people to contracts when they are that extreme.

It happens. We’re in a sensitive business, one where people are coming from all facets and stages of life — elderly folks looking to move into assisted living, divorcing couples who hate each other, children of recently deceased parents who are being bombarded with marketing and spam, people who love THINGS instead of people and collect items that fill up every room of their home to fill the empty void in their hearts and souls (worse – it could be CATS!), etc. and so on.

The question becomes how do we, as real estate problem solvers and marketers, KEEP GOING after hearng NO, experiencing REJECTION time and again, and then having deals that explode and turn into big wastes of time and effort? How do we keep going to that NEXT call back, helping that NEXT person who needs us when it’s almost CERTAIN we’ll be stomped on again and again?

Whoa! Did you feel the weight of what I just wrote? [Moment of silence.]

Ok, first, you need to remember that NEW SELLERS HAVE NO KNOWLEDGE OF YOUR LAST CALL/VISIT. Every single one of them has their own unique problem or reason for calling YOU. It’s up to YOU to find out WHY they need your services — and do NOT transfer the energy from any previous negative dealings into a new call or visit.

Imagine if your phone was completely flooded with calls, so that when one seller swears at you and makes you take them off your list, you need to let them go because you have another call coming in from a legitimate person who has already accepted their situation and they know they need you??

Different ballgame, right?

In any event, friends, be it real estate or any other business, we are in the sales business, and we need to smile and hold our heads up high the entire time. Sometimes the only thing we’ll have to rely on is our vision — our vision of helping sellers and the neighborhoods we’re investing in, the vision of our business we want to share with the community, and our vision of bettering our own lives and families — our businesses and missions are bigger and deeper than any amount of NOs or rejection we could go through.

And remember, if you’re here and doing this business as you should, you should feel MORALLY and ETHICALLY obligated to share your services because of how much good they are providing in your local communities. This is another reason why I treasure positive testimonials from my sellers and neighbors so much — when times get tough, THEY keep me going.

You got this. Wipe the sweat, blood, and tears from your face, and keep on changing lives.

https://aarealestategroup.com/wp-content/uploads/aa_real_estate_logos_final_group-300x112.png00Nick Aalerudhttps://aarealestategroup.com/wp-content/uploads/aa_real_estate_logos_final_group-300x112.pngNick Aalerud2016-09-21 15:15:032016-09-21 15:15:03How Do You Keep Going After “No!”?